Our team speaks “legacy planning” fluently. But we’re also about approachability and transparency, and we understand that it might seem awkward to stop a legacy planning conversation and ask what is probate? or how is a CRUT different from a CRAT? (Or, as one donor recently quipped, “‘cr-ut’ sounds weird. I’d prefer ‘cr-oot.’ Let’s say ‘cr-oot’ from here on out.’ We did. She created one, and her favorite charities will benefit from her “cr-oot” for years to come. To each their own!)

Back to industry jargon. It might seem like alphabet soup, but these definitions matter. Understanding key legacy and estate planning concepts is foundational to making the best decisions for your family, your life stage, and your philanthropic goals. Here’s a quick run-down of the words, phrases, and acronyms that probably roll off our tongues without us even realizing it. Look up the ones you’ve been wondering about, and set the record straight.

Adjusted Gross Income (AGI) – This is your total taxable income minus your deductions (charitable and otherwise) for the year, and it determines your tax bracket. In 2020, you can deduct up to 100% of your AGI thanks to the CARES Act.

Beneficiaries – These are the people or organizations that’ll receive trust income or other assets through your estate. They could be your kids, family members, friends, or other individuals…literally anyone! Or, one of the quickest ways to remember a favorite nonprofit in your plan is to name it as a beneficiary on a retirement plan, investment, or bank account. Beneficiary designations can be set up in minutes with your financial advisor or fund custodian…and they could help keep your assets from landing in probate, because they follow strict contractual guidelines specifying the person to whom the proceeds should be paid.

Bequest – A gift of money directed by a will, trust or beneficiary designation. It can be changed or eliminated from your plans if circumstances change.

Coronavirus Aid, Relief, and Economic Security (CARES) Act – Signed in March 2020, it includes a $300 deduction for charitable giving, even if you don’t itemize in 2020. This year only, you can also deduct up to 100% of your AGI (ahem – that’s Adjusted Gross Income). Up to 40% can be used to fund a Donor Advised Fund (DAF).

Charitable Lead Trust (CLT) – It’s an irrevocable trust fund that distributes an annual payout to a charitable organization for a specific number of years, then passes the remaining principal (and any potential growth) back to the grantor or beneficiaries. Because the annual payout to charity is tax deductible, it can help reduce taxes while ultimately passing ownership to family members or other beneficiaries. Funding a CLT with assets that are expected to increase in value can be an important tax minimization technique. But because a CLT is irrevocable (i.e. it can’t be changed or cancelled if circumstances change), family members will not have access to or benefit from the trust property until the trust term expires.

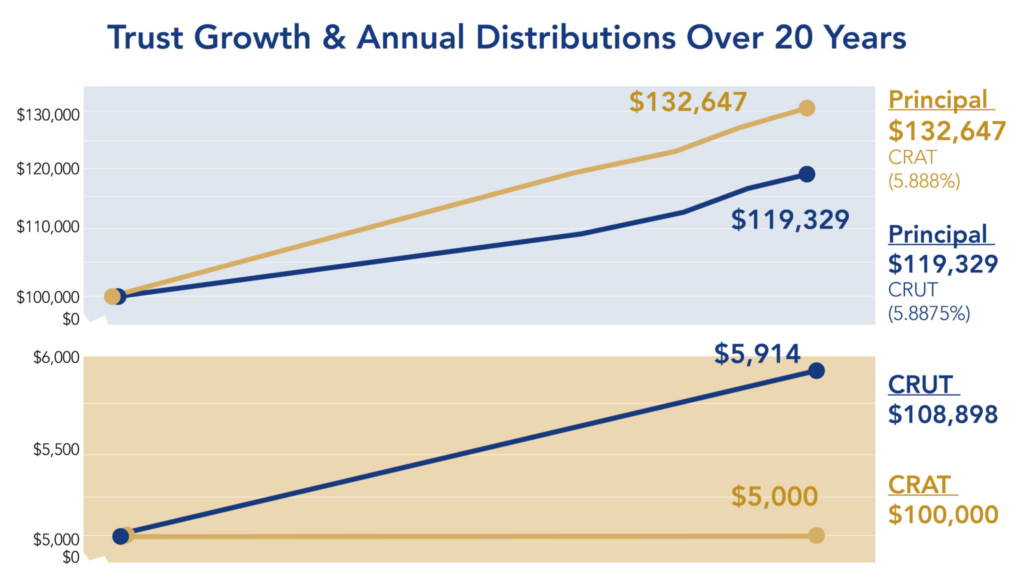

Charitable Remainder Trust (CRT) – this type of trust provides income for the donor, spouse, or other beneficiaries before making a substantial charitable donation. It’s kind of like the reverse of a CLT. Once it is funded, it becomes an irrevocable trust that pays non-charitable beneficiaries (like a spouse, child(ren), or grandchild(ren)) income during the trust term and then gifts the remainder to qualified 501(c)3 charities or ministries. The value of the charitable remainder must be at least 10% of the initial value of the property transferred to the trust.

There are two main types, and the major difference is how payments are made to the donor/heirs:

Charitable Remainder Annuity Trust (CRAT)

Irrevocable (permanent) trust that pays out a consistent, specified percentage of the initial value of the trust assets. So, each payment is the same amount and can be a consistent source of income to the donor or heirs.

*Helpful hint: think of the “A” in CRAT as standing for “always remains the same.” The payment never increases, even if there is a large gain in the trust. One downside is that it’s possible to exhaust the trust if the market drops significantly. The trust is still required to keep paying heirs, and there may not be a remainder gift to charity at the end of the term. (If the payment to the heirs uses up all of the remaining balance of the CRAT, payments to the heirs will cease and there will not be a gift to charity.)

Charitable Remainder Unitrust (CRUT)

An irrevocable (permanent) trust that pays a specified percentage of the current value of the trust assets. This means the payment changes each year.

*Helpful hint: think of the “U” in CRUT as standing for “up or down.” The payment to yourself/family/heirs can go up or down, depending on the value of the trust. If markets go up, heirs receive a larger pay-out. If the market value of the assets of the trust go down, heirs’ payments get smaller. This type of trust can’t be outspent, so there is always a gift left to charity at the end of the trust term.

Check out this helpful graphic that shows the difference between CRATS and CRUTS:

A Donor Advised Fund (DAF) can be thought of as your “charitable checkbook.” The donor makes a charitable contribution to a sponsoring organization, which then owns the assets and administers the fund. The donor receives an immediate income tax deduction for the contribution, but the fund can be invested and can grow or shrink. The donor retains control of the charitable funds in the account, and can decide how, when, and where to make grants. DAFs are incredibly flexible and versatile, because a donor can give what is most favorable at the time that works best for them. Additionally, a DAF may allow the donor to maintain anonymity–or at least minimize publicity–when they choose to give.

An Executor (also referred to as a Personal Representative) is an individual or corporation chosen by the testator to oversee administration of the estate. They collect and inventory assets and pay debts, taxes, funeral costs, and other eligible expenses. They also handle any claims or disputes, and ultimately distribute the assets in accordance with the directives made in the will. We have a whole blog post coming soon about what makes a great executor…but in general, this person should be organized, honest, and respected by the beneficiaries.

Funding is the process of transferring assets you personally own into the name of your trust. This can be done during life or at death. If funded properly during life, you may avoid any probate costs on the assets transferred into the trust. If funded at death, you may still have the “opportunity” to pay the probate fees associated with transferring the asset to the trust.

A Grantor is the individual who puts his or her property into a trust.

Guardian (short for “Guardian of the Person and/or Guardian of the Estate of Minor Children”…how’s that for a mouthful?) The guardian of the person is the individual (or individuals) responsible for the care, custody, and upbringing of a minor. The guardian of the estate is an individual, multiple individuals, or corporation responsible for the financial affairs of a minor child. Once a child reaches the “age of majority” (meaning they are legally an adult; age 18 in all states except AL, MS, and NE), then the guardian no longer has authority to make decisions, and that child will receive full control over his or her property, unless provisions of the will, trust, or other estate planning documents state otherwise. The guardian of the person and the guardian of the estate are often the same individual(s), but not necessarily.

Immediate Power of Attorney – As opposed to a “springing power of attorney,” this role takes effect immediately.

Intestacy (or to “die intestate”) is the term for the default set of rules that govern the distribution of an estate when a person dies without a will. These rules–which are outlined in each state’s laws–distribute the assets of an estate based on family relationships only. These laws don’t consider any special circumstances, friends, charities, or any other factors that a donor may consider when creating a will. Additionally, no consideration is given to minimizing taxes or estate costs…all told, you don’t want to die intestate! Your own customized plan, even a basic one, is always the better option.

Individual Retirement Account (IRA) – There are a few different kinds, but in general, it’s a tax-deferred investment fund set up by the individual, not their employer. A gift given through an IRA Rollover can be a very tax-efficient way to support charity later in life!

An Irrevocable Trust, once created, can’t be changed by the grantor. In fact, the grantor surrenders all ownership to property that is placed in an irrevocable trust.

Irrevocable Life Insurance Trust (ILIT) – An irrevocable (permanent) trust established in order to purchase and hold a life insurance policy for the donors, who are beneficiaries of the trust and will receive the proceeds under the trust terms. The ILIT keeps the life insurance policy out of the donor’s estate for federal tax purposes and provides protection from creditors (in case that becomes an issue in the future).

Joint Tenancy (short for “joint tenancy with rights of survivorship,” also known as “co-ownership”) – a shared right to property, or situations where two or more persons have concurrent ownership of an estate. They’re regarded as a single owner, and in theory, each owns the undivided whole of the property. So when one joint tenant dies, nothing passes to the surviving joint tenant(s). Rather, the decedent’s interest is extinguished, and the estate simply continues with the survivors having equal undivided shares, identical interests, and right to possession of the whole estate. Sometimes people refer to this as the “last man standing” model of survivorship, because at death of a joint tenant, his or her portion is evenly redistributed to remaining joint tenants and the last to die becomes the sole owner of the property.

Payable on Death (POD) accounts provide for some or all the assets in a bank account to pass directly to specific individuals upon death, outside of probate. If directed by POD, the will has no control over the accounts.

Personal Representative (see “Executor”)

A Pour-Over Will names a guardian for minor children and protects against intestacy if there are any assets that haven’t been transferred into the trust at the death of the settlor/trust-maker.

It’s used in tandem with a revocable trust, and serves as a “safety net” by instructing the executor to transfer any unaccounted-for assets to the trust so that everything can be settled as a single, cohesive whole. However, it does not avoid probate if the aggregate value of the assets passing by the will exceeds $50,000 (depending on the state), or if there is any real estate. So it’s very helpful for all assets to be properly titled in the trust!

A Power of Attorney for Health Care allows a person (the “principal”) to delegate to another person (the “agent” or “attorney-in-fact,” often a family member or friend) the power to make health care decisions on their behalf if he or she is unable to make such decisions. It permits the principal to provide instructions regarding medical treatment: basic or advanced medical procedures, the withholding of food and fluids, and the use of life- prolonging treatment. If an individual does not have a power of attorney for health care and then becomes incapacitated, a guardianship proceeding may be necessary to appoint someone to make health care decisions. This process can be long and expensive, and has an emotional cost, especially if family members disagree as to who should be elected as guardian or how health care should be handled.

A Durable Power of Attorney for Legal & Financial Matters allows a person (the “principal”) to delegate to another person (the “agent” or “attorney-in-fact”) the power to make decisions regarding the principal’s assets, finances, bank accounts, and other types of property. It can be revoked at any time and its power automatically ends upon the death of the principal. Like with the power of attorney for health care, If an individual does not have a power of attorney for property or a funded revocable trust, and then becomes incapacitated, a court proceeding may be necessary to appoint a guardian to act on his or her behalf.

A Power of Attorney for Legal & Financial Matters is the same as the Durable Power of Attorney, but is usually only good for a specified period of time or even during a specific event. For instance, if you are going to be gone from the country for an extended period, you may want to delegate a power of attorney to act on your behalf for any legal or financial transactions.

Probate Process Probate is a legal process in which a probate court settles the estate of a deceased individual (the “decedent”). The process of probating a decedent’s estate involves gathering and accounting for the assets of the decedent, payment of debts, taxes, claims and costs of administration of the decedent and distribution of probate assets to the beneficiaries. Typically, assets that are subject to the probate process consist of real estate, financial assets, and personal property titled solely in the decedent’s name at death, which do not pass automatically to a third party upon the decedent’s death. Probate generally involves paperwork and court appearances. Any fees and court costs are paid from estate property, reducing the amount which would otherwise go to the decedent’s beneficiaries. Formal court-supervised probate can be a costly, time-consuming process. In many cases, the less formal and simpler “independent administration” can be used to streamline this process. The cost of probate is either set by state law or by practice and custom in your community.

A Revocable Trust (also known as a living trust, revocable living trust, or inter vivos trust) is a trust funded during the trustee’s lifetime. It lets the grantor change the terms, add or remove property, or even (as the name implies) revoke the trust entirely. In estate planning, we talk primarily about revocable living trusts, because they offer the greatest amount of flexibility if circumstances or family dynamics change. But keep in mind there are many other forms of trust, and that can be cause for confusion!

A Settlor (or Trust Maker), is an individual that establishes the trust and determines how it will operate.

“Springing” Power of Attorney – this role is effective upon the occurrence of an event or upon the incapacity of the principal for the Springing Durable Power of Attorney.

A Testator is the individual that creates a last will and testament to dictate their wishes for the transfer of assets at their death.

Transfer on Death (TOD) accounts (also known as Totten Trusts) provide an alternative to jointly-owned assets for bank accounts. During lifetime, the beneficiary of the TOD account has no rights to the account. The beneficiary/beneficiaries can be changed at any time by the account owner, the funds can be spent, or the account can be closed. At death, the asset is transferred to the beneficiary without going through the probate process.

A Trustee is an individual (or a corporation or bank) who keeps legal title, possession, and control over the trust property. The basic duties involve collection, management, and investment of trust assets, and the accumulation and distribution of income and principal to beneficiaries, all pursuant to the terms of the trust agreement.

Trust Maker (see Settlor).

If we think of the will as the basic “road map” for an estate, a Trust is like an “atlas.” It’s a legal entity created by the grantor to contain property. A trustee then manages that property for the benefit of the beneficiaries. Some specific types of trusts are: Charitable Trusts, Charitable Remainder Trusts, Charitable Lead Trusts, Minor’s Trusts, Spendthrift Trusts, and Special Needs Trusts.

Trust Property refers to the assets–or “corpus”–held within a trust. These assets may include almost anything capable of being legally owned, such as real personal property or a contract right such as a life insurance policy.

Trust Terms refer to the instructions detailing the trustee’s duties and the eventual distribution of assets. A trust provides the grantor with a degree of control that is not possible with a simple will–in particular, the ability to control and distribute assets after death through the trust terms.

Taxation of Trust Income – Income taxes are due on income generated by trust assets. For this reason, people generally prefer to put non-income-producing assets into trusts—assets such as growth stocks that don’t pay dividends, or tax-free municipal bonds. It’s also common to transfer life insurance policies to a trust. It is important to note that you will not be saving any taxes when you place assets into a trust (unless it is a charitable trust in which the assets grow tax-free). In fact, a trust jumps up to the maximum tax rate of 37% federal income tax once the trust earns over $12,950 per year. This is important to note when putting assets into a trust and when deciding on what type of trust is the best option for you.

A Will is like a “road map” of a donor’s estate–a legal document created under state law in which the donor defines his or her intentions for the distribution of the estate. To do this, a testator makes bequests of specific property (i.e., stock, money, jewelry, a car, etc.) to specific individuals.